This table does not include all companies or all offered items. Interest does not back or suggest any business. Editorial Policy Disclosure Interest. com abides by strict editorial policies that keep our writers and editors independent and sincere. We count on evidence-based editorial standards, routinely fact-check our content for precision, and keep our editorial staff completely siloed from our advertisers. If the rate were to increase 1 basis point, it would increase to 3. 26%. If it were to increase 50 basis points, it would increase to 3. 75%. A 100-basis point increase would result in a 4. 25% rate. If a loan rate is 5% and goes up 20 basis points, that is the equivalent of raising the rates of interest by 0.

2%. If rate of interest are at 4. 75% and drop to 4. 6%, that is a 15-basis point (0. 15%) decrease. Although a basis point seems small, even a modest change can make a huge distinction in the total interest you pay over the long term. Here is a chart demonstrating how total payments on a $200,000 loan modification, based upon a 30-year fixed home mortgage of 3.

75%-- $926. 23 $333,444 $133,444 3. 85% 10 points $937. 62 $337,541 $137,541 3. 95% 20 points $949. 07 $341,668 $141,668 4. 25% 50 points $983. 88 $354,197 $154,197 * Rates are for example only. Your rate will depend on current home mortgage rates plus your credit rating. Don't confuse discount rate points (typically just called points) with basis points.

For instance, a point on a $200,000 loan would equal $2,000. When you pay discount points, you're basically prepaying a few of the interest on a loan. The Click here for more more points you pay at closing, the lower the rate of interest will be over the life of the loan. This can help make monthly payments more budget-friendly and conserve money in interest over the long term.

Portfolio managers and financiers use basis indicate indicate the portion change in interest rates or financial ratios in U.S. Treasury bonds, shared funds, exchange-traded stocks and genuine estate-based investments. Experts utilize mathematical terms to explain basis points but even if you're not a financial analyst or lender, you can understand them, too.

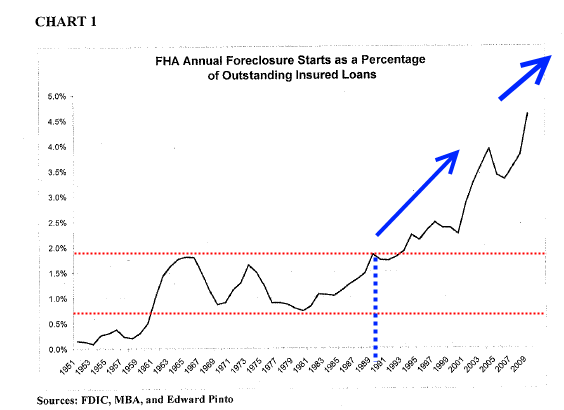

Facts About How Often Do Underwriters Deny Mortgages Revealed

One basis point equals 0. 01%, or 0. 0001. One hundred basis points equates to 1%. How does this translate to home loans? Let's state you have an adjustable rate home loan (ARM). Your rates of interest is 3. 50%, then the interest rate changes to 3. 75% at a later date. This implies your rates of interest rose by 25 basis points.

You'll hear the term "basis https://canvas.instructure.com/eportfolios/128899/juliusmxlv539/Little_Known_Questions_About_Which_Of_The_Following_Are_Banks_Prohibited_From_Doing_With_Highcost_Mortgages points" frequently utilized in connection with home loans (how did subprime mortgages contributed to the financial crisis). One basis point is 1/100 of 1 percent. While definitely not a large percentage amount, basis points can be exceptionally essential in home mortgage circumstances. Because of the size of home loan, basis points although little numbers - what is an underwriter in mortgages. When you hear or check out an increase/decrease of 25 basis points, you need to know this indicates one-quarter of 1 percent.

01 percent in interest. what are today's interest rates on mortgages. Particularly crucial to large-volume mortgage loan providers, basis points-- even simply a couple of-- can imply the difference between earnings and loss. Economically speaking, mortgage basis points are more crucial to lenders than to borrowers. Nevertheless, this effect on lending institutions can likewise impact your home loan interest rate.

25 get rid of timeshare or 0. 375 percent their used home mortgage rate to customers perhaps you. Basis points are popular with bigger financial investments such as bonds and home mortgages because. Unless you operate in the world of financing, you may not be aware of the appeal of basis points (what to know about mortgages in canada). From a mortgage viewpoint, little boosts in basis points can mean bigger changes in the rate of interest you might pay.

When you compare home loan rates and terms, you will ultimately experience basis points. For example, you speak to a loan officer, informing him/her that you want to lock-- guarantee your rate at closing-- your rate for 60 days. The loan officer then encourages you that the loan provider charges 50 basis indicate lock your rate for that period.

Fascination About Which Of The Following Is Not True About Reverse Annuity Mortgages?

Home loan rates tend to "lag" be a bit behind other market rate of interest. Understanding basis points might help you, to a degree,. If you are nearly prepared to make a mortgage application, understanding of basis points may help you save some cash. For example, you notice bond yields and costs increased by 20 basis points on Monday.